Oregon Pacific Bank Announces First Quarter Earnings Results

Florence, Ore., April 18, 2023 – Oregon Pacific Bancorp (ORPB), the holding company of Oregon Pacific Bank, today reported financial results for the first quarter ended, March 31, 2023.

Highlights:

- First quarter net income of $2.4 million; $0.34 per diluted share.

- Quarterly loan growth of $10.5 million or annualized growth of 8.82%.

- Quarterly deposit growth of $7.2 million or annualized growth of 4.26%.

- Quarterly tax equivalent net interest margin of 3.87%

View full earnings release with financial tables: MAR-Statement-of-Condition-Q1-2023.pdf

Net income for the quarter ended March 31, 2023, was $2.4 million, or $0.34 per diluted share compared to $1.4 million or $0.20 per diluted share for the quarter ended March 31, 2022. Ron Green, President and Chief Executive Officer said today upon the release of Oregon Pacific Bank’s earnings, “We are pleased with our first quarter results for 2023, reflecting period-ending, year-over-year growth in net loans, deposits, and earnings per share.” He continued, “During the recent events surrounding the closure of two larger financial institutions in the United States, our historical emphasis on balance sheet diversification, and our focus on attracting business banking relationships that value service, continues to serve the Bank well. Our increase in cost of funds has been at a rate lower than most of our peers. Although we are aware that some business depositors have invested their excess liquidity in non-banking products, such as U.S. Treasuries, we have not lost any business relationships to other local or regional commercial banks purely for reasons of clients demanding a higher yield on deposits. We will continue to lead with our value-proposition of service first and our desire to create mutual value for the Bank and its customers.”

Period-end loans, net of deferred loan origination fees, totaled $493.5 million, representing quarterly growth of $10.5 million. The first quarter loan yield grew to 4.85%, an increase of 0.15% over the prior quarter. Effective January 1, 2023, the Bank adopted Accounting Standards Update 2016-13, Financial Instruments – Credit Losses (Topic 326), Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”) and all related amendments. The day 1 adoption of ASU 2016-13 and related amendments resulted in an increase of $60 thousand to the Bank’s allowance for credit losses on loans, an increase of $777 thousand to the Bank’s allowance for unfunded commitments and letters of credit and a net-of-tax cumulative-effect adjustment of $611 thousand to decrease the beginning balance of retained earnings. The Bank’s estimate of provision for credit losses for the first quarter of 2023, under the new CECL methodology, resulted in a reversal of $51 thousand of provision expense, which was comprised of an increase to the allowance for credit losses on loans of $70 thousand and a reduction in the reserve for unfunded commitments of $121 thousand. In addition to provision for credit losses, the Bank also recognized recoveries of $88 thousand during the quarter.

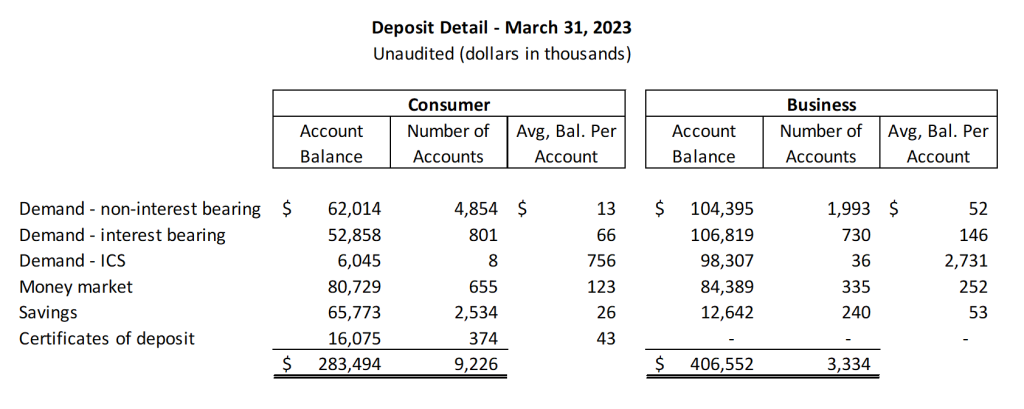

The Bank experienced quarterly deposit growth totaling $7.2 million or an annualized increase of 4.26%. Included in the first quarter deposit growth was approximately $19.1 million in deposits that migrated from off-balance sheet holdings with IntraFi Network, into on-balance sheet reciprocal balances. As of March 31, 2023, the Bank has migrated all off-balance sheet deposits into a reciprocal position. During the quarter the Bank experienced an increase in requests for the full FDIC insurance coverage associated with the Insured Cash Sweep accounts. Excluding the reciprocal migration, the Bank’s ICS balances grew $22.5 million. The ICS balances are currently listed under the demand interest bearing category on the balance sheet. As deposit rate pressure continues, the Bank’s cost of funds increased to 0.51% during the first quarter 2023, up from the 0.21% reported in the fourth quarter 2022. The Bank has also analyzed deposit balances and below is a breakout of deposit balances as of March 31, 2023, by type.

The securities portfolio contracted slightly from $195.9 million at December 31, 2022, down to $195.6 million at Mach 31, 2023. The contraction was attributable to portfolio cash flows, which was partially offset by a reduction in the unrealized loss on the portfolio, as the Bank did not purchase any securities during the quarter. The unrealized loss at March 31, 2023 reflected a reduction of $1.9 million, moving to $12.4 million, down from $14.3 million at December 31, 2022. The increase in market values was primarily attributable to a reduction in longer-term interest rates positively affecting the market values. The weighted average life of the portfolio was 5.2 years and the modified duration of 4.4 years at March 31, 2023. During the quarter the yield on securities grew to 3.41%, up from 3.02% in the fourth quarter 2022, with securities income increasing $217 thousand over fourth quarter 2022, which was primarily attributable to the securities repositioning strategy executed during fourth quarter 2022.

Noninterest income totaled $1.7 million during the first quarter 2023 and represented a decrease of $187 thousand from fourth quarter 2022. The largest decrease in noninterest income occurred in the other income category, which is primarily attributable to the income earned on the off-balance sheet portion of the IntraFi Network deposits, which totaled $7 thousand during first quarter 2023, down from $191 thousand in fourth quarter 2022. With the Bank migrating all IntraFi deposits into a reciprocal position, this source of noninterest income is not anticipated in future periods.

First quarter 2023 noninterest expense totaled $5.3 million, down $1.4 million from the $6.7 million recorded during fourth quarter 2022. During the fourth quarter 2022 the bank recognized a loss on sale of securities of $1.8 million. Excluding the loss on sale of securities, noninterest expense increased $405 thousand over the fourth quarter 2022. The largest fluctuation occurred in the salaries and employee benefits category which grew $342 thousand, primarily attributable to the full quarter of salary expense associated with the Portland Market expansion.

Forward-Looking Statement Safe Harbor

This release contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 (“PSLRA”). These statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements often use words such as “anticipates,” “targets,” “expects,” “estimates,” “intends,” “plans,” “goals,” “believes” and other similar expressions or future or conditional verbs such as “will,” “should,” “would” and “could.” The forward-looking statements made represent Oregon Pacific Bank’s current estimates, projections, expectations, plans or forecasts of its future results and revenues, including but not limited to statements about performance, loan or deposit growth, loan prepayments, investment purchases, investment yields, strategic focus, capital position, liquidity, credit quality, special asset liquidation, noninterest expense and credit quality trends. These statements are not guarantees of future results or performance and involve certain risks, uncertainties and assumptions that are difficult to predict and are often beyond Oregon Pacific Bank’s control. Actual outcomes and results may differ materially from those expressed in, or implied by, any of these forward-looking statements. You should not place undue reliance on any forward-looking statement and should consider all of the following uncertainties and risks. Oregon Pacific Bancorp undertakes no obligation to publicly revise or update any forward-looking statement to reflect the impact of events or circumstances that arise after the date of this release. This statement is included for the express purpose of invoking the PSLRA’s safe harbor provisions.